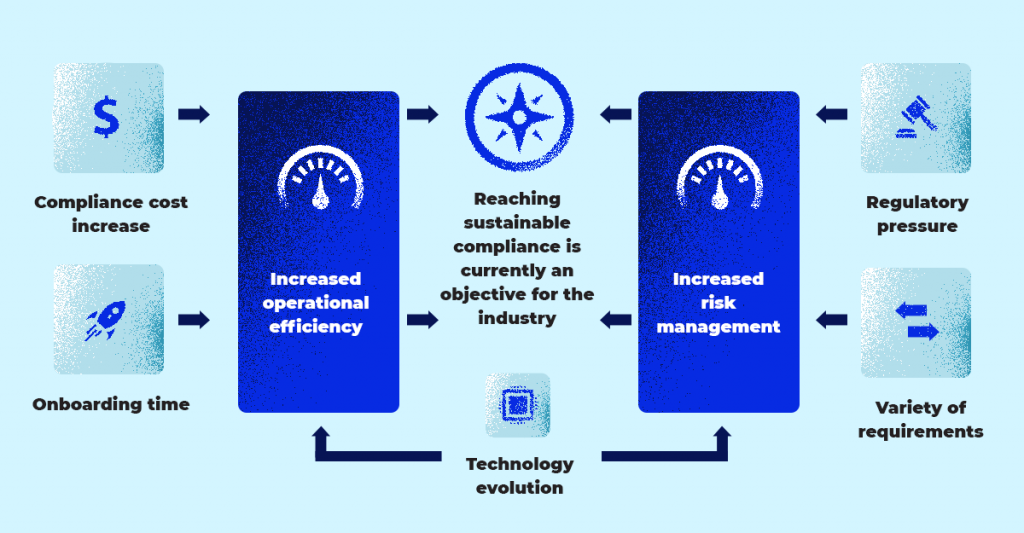

As digital finance is gaining traction, the KYC (Know Your Customer) process is becoming vital for sustainable business models. With regulatory compliance at the roots and modern software solutions in all branches of operation, FinTech’s evergreen status relies on striking the right balance between code of conduct and customer experience. While tapping into the ABC of KYC, we begin our due diligence by identifying industry leaders in digital identity verification for financial services.

The ABC of KYC

A: All shall comply

A web of regulations binds all financial institutions as responsible for customer due diligence (CDD) to prevent fraud and money laundering (AML). FinTechs carry this burden of proof with grace, despite the volatility of both the regulatory landscape and cybercrime. PSD2 and GDPR directives are examples of how compliance standards and data protection are handled in the European Union. However, as cryptocurrency and crypto asset transactions are on the rise, we might expect much more legislative pressure on risk management in all verticals of the finance industry.

B: Biometrics of identity

While lawmakers battle fraud with an outpour of regulations, RegTechs offer innovative and practical Customer Identification Programs (CIP). Digital onboarding often involves cutting-edge software solutions and technologies:

- blockchain (decentralised ownership of data & quick auditing)

- AI (self-learning algorithms to approve documents)

- biometrics (face & voice recognition using biometric features)

- streaming (ID & liveness checks via video chat)

Because both regulations and data attributes are subject to constant change, KYC systems need to be scalable and dynamic. Moreover, compatibility issues of the API framework can become particularly dire in the case of cross-border transactions.

C: Customers on board

Effective KYC policy can be a competitive factor. In the spirit of UX, bad experience at this stage of interacting with a digital product means users may never give it a second chance. What’s more, the gathered data can provide valuable insight on the use of services, (e.g. tracking customer transaction behaviour). Accurate risk assessment also helps build transparency and mutual trust: the cornerstones of customer relations. On a similar note, competent data protection paired with efficient credit scoring give users a sense of security, which makes digital lending and trading possible (especially in P2P ecosystem).

KYC providers: Hall of fame

The three pillars of KYC outlined above are just a taste of the complexity and significance of digital identity verification in financial services. Meanwhile, four companies have caught our eye as particularly successful in navigating the maze of regulations and tech-driven compliance.

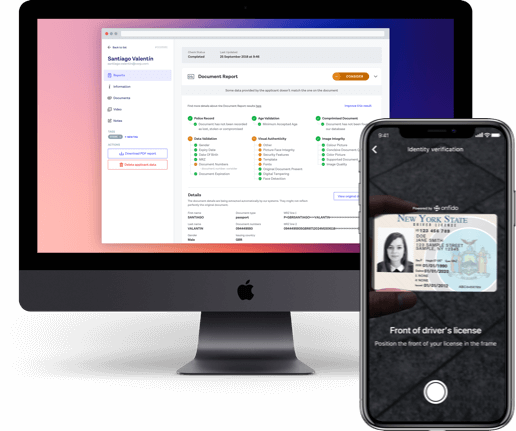

Onfido

What’s the catch?

Onfido advocates its hybrid approach to document verification (combining AI, machine learning and human analysis) catches up to 98.7% of ID fraud attempts. This impressive accuracy is accompanied by a wide coverage of geographies (4,600 types of documents from 195 countries), languages and scripts. Additional trivia include a strategic partnership with Interpol and advisory activities benefiting governments, border security and document printing entities.

Claps for UX

Focus on user experience gives Onfido the edge among tech-savvy KYC and AML service providers. The company not only ensures that digital onboarding is fast and smooth, but also gives users real-time feedback. Examples of UX mindfulness include glare & blur detection and OCR Autofill of ID data during sign up. Onfido didn’t go unnoticed by FinTech giants, with Revolut pointing to a 12% increase in onboarded customers and LandInvest achieving an average pass rate of 97%.

Unit21

Standing strong

Headquartered in San Francisco, Unit21 is working with leading FinTechs, like Intuit and Coinbase. Its powerful technology has the backing of major VCs (including $3M from Google’s Gradient Ventures). The company is on a mission to put an end to organized crime by targeting money laundering on financial platforms. Having joined forces with other leading KYC providers, crypto blockchain forensics and third-party risk sources, Unit21 has your back on all fronts.

Full package

Above all, Unit21 is not just one solution, but a whole system for detecting suspicious activity, including applications for KYC, transaction monitoring and case management. Its AML software is accessible to risk analysts through a simple API enabling fast integration and a dashboard with multiple customization options. What makes Unit21 stand out is the way it empowers users with complex analytics and provides instant, ongoing support of its product team via Slack.

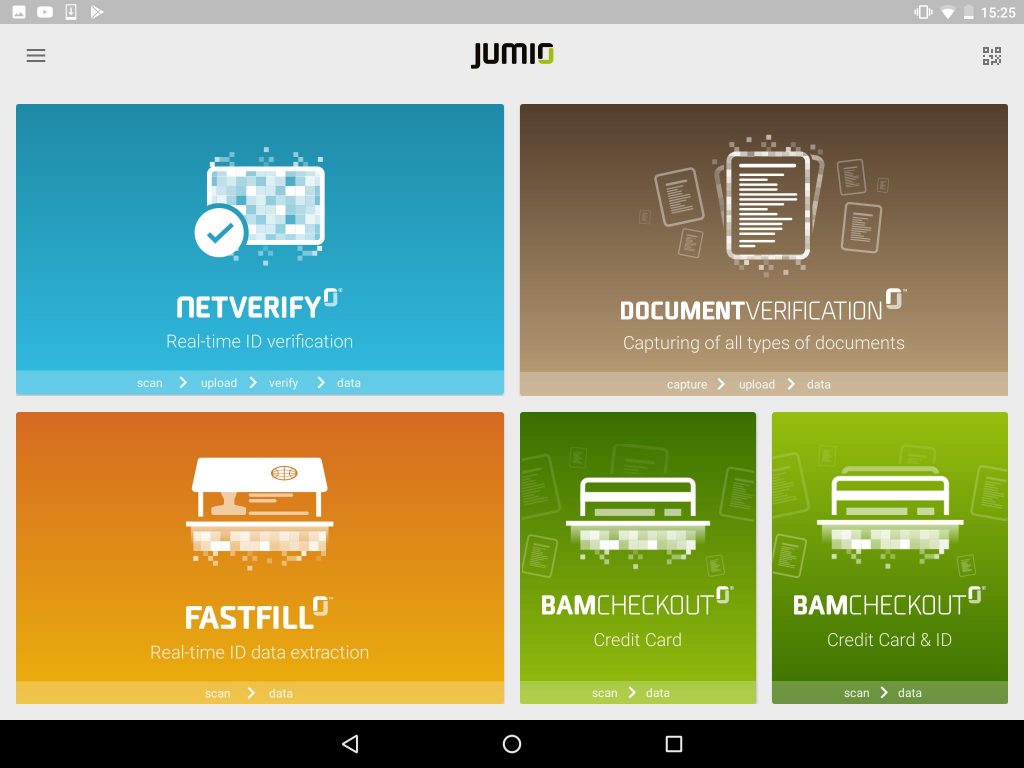

Jumio

You can bank on it

Praised by Monzo and HSBC, Jumio offers a solid KYC know-how for financial services with strong focus on remote onboarding and online identity verification. According to Jumio, the momentum of the signup process is key. That’s why their approach to boosting conversion highlights near real-time ID verification and data extraction to automate filling in registration forms. Other advanced FinTech options include securing high-risk transactions with biometric authentication.

War on fraud

Jumio claims to be “loved by users and loathed by fraudsters”. Much of it has to do with the ‘informed AI’ the company has been perfecting by incorporating large data sets and intelligent tagging. Results? Faster and more accurate ID verification with less built-in bias. Topped off with a certified 3D Liveness Detection and self-learning algorithms to spot anomalies, Jumio’s suite of products is a mighty weapon against cybercrime.

NorthRow

API-first

NorthRow’s single API for client onboarding and monitoring is worthy of appreciation by development teams and executive boards alike. This means not only seamless integration and sandbox testing but also full control over client data, complete with enhanced automation and scalability. Happy clients taking advantage of its RemoteVerify solution include Bankable, CashFlows, Modulr, and Open Banking.

FinTech Taskforce

With clients all over the UK FinTech scene, NorthRow deserves a special mention for its support of local SMEs in the recent crisis. A special FinTech Taskforce combines the company’s expertise in KYC/AML and KYB with lending and credit services from Trade Ledger, WiserFunding and Nimbla. Together, they have formed a lifeline of funding for companies most affected by Covid-19.

“On the Internet, nobody knows you’re a dog”

Regulatory compliance has high priority in the FinTech ecosystem and companies spare no investment in KYC solutions. What’s more, the ongoing digitisation of financial services will probably drive the demand for years to come. However, transparency and security can be seen a double-edged sword with great expectations on both sides of the user interface. That’s because digital identity might soon become the most desirable reliability currency in the digital-first world of future finance.