FinTech apps heavily rely on connecting with customers. They thrive by offering custom services to users bored and tired by classic banking. The more you know about your customers, the more you can give to them. The same works for prices – price optimization through machine learning is the ultimate tool for growing revenues. How is it done and what can you learn from existing examples?

Setting up the right price is tricky. Especially with a new product, and when you want to attract people, and highlight its value. Limiting access by building a high wall with the “Expensive” phrase on it doesn’t always pay off. That’s when machine learning algorithms come in. By analysing massive amounts of data, you can establish a competitive pricing strategy. How?

How can you use machine learning to make optimal pricing decisions?

There are few clear benefits that go beyond optimizing pricing models. Implementing the solutions below will transform the product almost in real-time. Not only if you’re an established company with a hit product. They are valuable for startups as well. Think of them as a very practical guide towards designing an app from the get to, with specific features and customer-facing solutions in mind.

This is how you can improve pricing models and management revenue:

- Use machine learning to process historical data and discover underperforming services in your app. There are FinTech products that offer one thing. Loans for example, often in a buy now-pay later model. There are, however, applications so popular among millions of users, that sell multiple solutions to the same audience. Which brings the most money to the table? Which can be used as a vehicle to make an A/B test for your discount policy? By digging through mountains of data, you can figure out what works and what doesn’t. This solution can free up resources (money, employees’ time) to pursue more profitable venues.

- Use automated pricing models to drive up total revenue by 5%. Don’t take our word for it – trust data. The Boston Consulting Group conducted a study and you can find its findings here. Optimizing pricing for products delivered a noticeable change in money flow. The company believes that machine learning offers optimal pricing rules in revenue management systems. It also enforces contractual pricing.

- Utilising automated pricing solutions gives insight on changing customers’ behaviours. In addition, it offers first-hand context on transactional data, providing the necessary perspective. One of the companies that offer interesting solutions is Vendavo. Their model and industry integrations work great with custom software development, powering your app. This particular combo can help you in making pricing decisions, especially based on cross-border parameters.

- Machine learning can tell you how much users are willing to pay for a product or a specific feature. This is done by correlation. You can pull information by linking spendings or monthly fees in a software-as-a-service (SaaS) model with discounts, promo codes, etc. It’s especially valuable in the case of VIP pricing plans and a model called “pricing grandfathering”. It’s a situation where a customer gets a flat and low price for the guaranteed functionality of an app, as long as they’re committed to being a paying customer on a monthly basis.

- Create user personas and attach AI-based propensity models to them, in order to predict your pricing’s impact. A propensity model is basically a chance of likelihood. In that bounds, you try to predict whether a first-time user or a paying customer will perform a certain and desirable action. It heavily relies on predictive analytics, which is nowadays fueled by machine learning algorithms. Thanks to propensity models you canincrease the customer retention and reduce churn.

- Improve the effectiveness of CPQ (configure, price, quote). Machine learning provides greater accuracy of prediction. That helps increasing profit margins, optimising overall pricing models and decreasing sales and promotional costs. An article by McKinsey shows how advanced analytics drive software pricing recommendations. It’s especially true when we consider dynamic deal scoring indexed to discounts. It provides the knowledge necessary to determine what level of discount you can offer to maintain a profit margin.

- Use rule-based artificial intelligence (AI) models to establish the risk-to-revenue. Software development, specially dedicated to the B2C market, isn’t always fully predictable. Customers’ needs and the market itself change rapidly. Friction in user experience can be managed but what about mobile app development? You can use the customer even before you know about the issue. The price is not acceptable. The solution is brilliant, but underdeveloped. Microcopy inside the app doesn’t transmit the offers very well. User experience design and user interface design are not attractive enough. Machine learning pricing algorithms won’t give you all the answers, but they can show you the right direction.

- Utilise user photo authentication, voice recognition and analysis, automatic photo tagging, and image matching. One of the biggest advantages of FinTech is that people can use banking services from anywhere in the world, any time they want. No or minimal paperwork. Post a claim, get the money, spend the money. It’s an example from the InsurTech sector but it works for the whole industry. Companies now use a large variety of tools to successfully identify users, and assess claims.

How to get this done?

If you’re still not hooked, let’s throw in some numbers. According to McKinsey, the estimated AI-based pricing solutions can have a global worth of $259.1B to $500B, globally. According to Mordor Intelligence, the AI market in the sector will grow from $7.27B in 2019 to over $35.4B by 2025. Those are, however, numbers you can’t use. As previously mentioned 5% is something real. How to get to that? Consider these factors:

- your customers’ personas

- your operating costs and preferred margins

- seasons and holidays

- economic variables

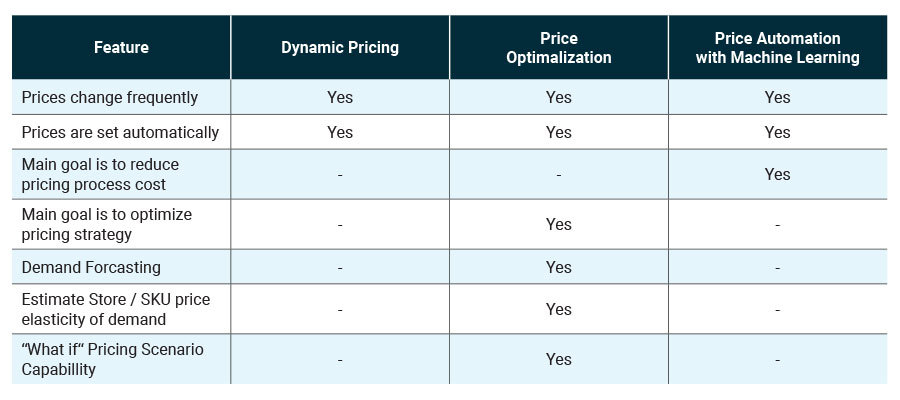

There’s also a thing called dynamic price. It’s adjusting prices, usually for a number of products, to react to the competition’s strategy. This model assumes frequent changes. It’s risky, unstable, and leads to churn. We have broken down the differences between price optimization, dynamic pricing, and price automation with machine learning:

Case study: Lemonade

Lemonade is an Israeli FinTech company that is built on and around machine learning. Their business model is based on a transparent fee that is plainly explained and open to everyone. 20% of income covers operational costs, the other 80% is used for claims, taxes, fees, etc.

The company’s success comes from utilizing various tools for prediction and analytics:

- satellite data from NASA for early detection of natural occurrences (not a joke!)

- chatbots for signups and claims handling

- a graph that builds connections between facts to help prevent frauds

- a virtual assistant called Maya for building tailored offers that customer receive

- a machine learning bot called Jim to analyze big portions of raw data. It’s used for building company policies, segmenting customers into risk groups and sharing in-house information about similar risk behaviors.

How does it work in everyday life? Maya pays claims in 3 minutes and insurance within a minute and a half. It also notifies users of nearby fires and other natural catastrophes and severe weather conditions. Maya is using Natural Language Processing (NLP) and Natural Action Synthesis (NAS). The bot is also using advanced CX.ai technology to make conversations with customers.

Jim, on the other hand, uses powerful machine learning algorithms to read and assess the nature of claims, spot “first notice of loss” factors and make payouts. In 2019 alone, Jim worked with 20.000 claims and paid around $2.5M. All without human involvement. Jim deals with user-generated data points and helps Maya in one ecosystem.

Is all of this 100% accurate? Of course not. That’s why Lemonade uses these bots, especially Jim, for two purposes:

- to help drive pricing policy

- to establish if a claim should be handled automatically or not

Price optimization is machine learning undercover

Competitors’ prices are their thing. Focus on what you’re doing. Massive amounts of data and machine learning can generate pricing recommendations but you still have to base decisions on your experience. Frankly, it’s about being a detective. Machine learning can and will give you a lot to think about, it can also free you from many mindless business operations. It can also be faulty.

That’s why it seems critical to still rely on humans who can oversee the bots. Bots can’t write, expand and adjust the software. They can’t design it. Finally, they can’t make a quality product by delivering specialists. Which the process of quality software engineering is really all about.