After finding the general landscape of FinTech in the Middle East so fascinating that I even had to present it to you in a blog post, I just had to select some of the most interesting examples of how technology changes lives in this region. You’ll be pleasantly surprised that very thorough curation in the accelerators there results in apps that are genuinely helpful and solve real-life problems! Read more to find out how.

After reading our last article about FinTech in the Middle East, you might be wondering what kinds of FinTech startups can be born there. Without further ado, let’s find out!

Nana

Country: Saudi Arabia

Service type: grocery shopping with home delivery

Nana is the number one grocery shopping service in Saudi Arabia right now and “thanks” to the COVID pandemics it’s growing extremely fast. The startup was founded in 2016 thanks to generous investors who offered USD 29 million to the company. Now, Nana cooperates with all major grocery chains and pharmacies (including Carrefour and Spar) and delivers to any place within supported cities (there are 14 of them now, but the company promises to cover as much of the country as possible very soon). What makes the app special is the super-approachable technical support which users can access 24/7 and an option of scheduling deliveries precisely and have them whenever you need.

Nana is proudly developed by a team of young Saudi entrepreneurs and employs a whole network of delivery specialists who personally pick high quality groceries for the customers.

NymCard

Country: United Arab Emirates and Lebanon

Service type: payment processing and card issuing

As a pretty fresh startup, NymCard is definitely a company worth watching in 2021. It was created during the pinnacle of the MENA banks modernization wave as a solution that makes distributing and controlling cards (both physical and digital ones) as smooth as possible. The whole system operates in the cloud and uses a number of open APIs to automate processes and make them perfectly secure (3D Secure authentication).

Why is NymCard a go-to solution for payments and card distribution in the MENA region, though? The company’s solution works in an end-to-end model, taking care of all security related problems (fraud prevention, permissions, reconciliation, data protection) in the background. It also allows the clients to operate a fully compliant product without actually having to take care of the compliance issues, as it’s all done on the NymCard’s side. Obviously, to achieve this all the company cooperates with major banks and even Visa.

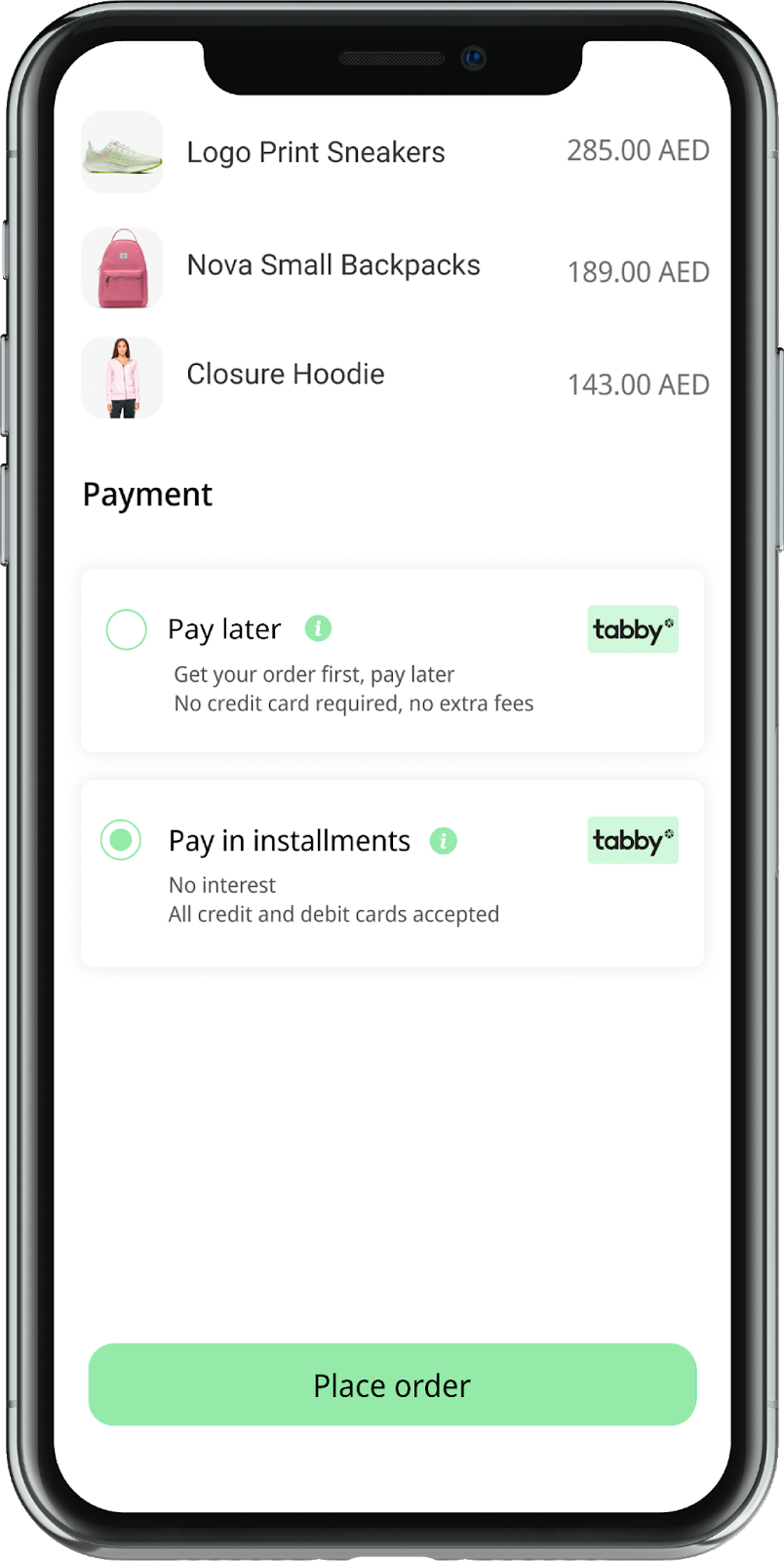

Tabby

Country: United Arab Emirates

Service type: buy-now-pay-later

Just as NymCard, Tabby is a freshly founded, yet quickly growing company (founded in 2019). Its main goal is to offer the buyers easy access to products in difficult financial times. How does it work? When buying online, you just choose Tabby on the checkout screen of a partnered-up store and decide whether you want to pay later or pay in installments (no interest charged). You can do the same while purchasing in-store. Just generate a QR code in the Tabby app and show it to the cashier – it’s dead simple.

But the service would be pointless if it didn’t offer a wide range of stores and ecommerces to choose from. Fortunately, there are literally hundreds of companies that accept Tabby, so Arabian customers are free to use it whenever they want.

Mamo Pay

Country: United Arab Emirates

Service type: P2P payments

Sending money to another person has never been easier in the Emirates. Thanks to Mamo Pay, you can send instant transfers or receive money without the need to manually generate bank transfers and without waiting for the ELIXIR session. Moreover, you can even split bills. The app can be connected to your credit card or bank account and, as all successful FinTech apps, is perfectly simple to use (see our UX design services). All you need to do to send money is pick the sum and choose the receiver. It can be anyone from your ordinary contact list, a phone number or email address is enough. As usually with similar solutions, you don’t need to worry about security – the startup was created in collaboration with Visa and within the Visa’s FinTech Fast Track Program.

Sary

Country: Saudi Arabia

Service type: B2B marketplace

It’s always difficult for small businesses to offer their products to large clients. Imagine you’re a local farmer and you’d like to supply your produce to an exclusive hotel. How can you reach such a client? The simplest way seems to be partnering up with a middle man. But it always reduces your revenues. Thanks to a marketplace, such as Sary, the clients can notice you and buy directly from you. The app is essentially a smart wholesale trade marketplace which makes the lives of the suppliers better and gives the clients easy access to a huge catalogue of goods at great prices. The platform also supports a number of payment options, such as cash-on-delivery, card payments and e-bill through Sadad (paperless transactions.)

Ajar Online

Country: Kuwait

Service type: real-estate management

Renting a flat always involves money. As a tenant, you need to pay your bills and as the owner, you need to collect rent. However, if you own a bigger number of properties and need to manage them efficiently, using a spreadsheet may be troublesome. Ajar Online solves most of the problems on both ends. As a landlord, you get clear insight into what is going on with your units, automatically send customized invoices, receive messages from the tenants (“The AC is not working” etc.) and generate detailed reports to optimize the business. As a tenant, you’ll receive alerts for due payments and will be able to realize them in a cashless way. The app has quickly become a hit among the leading real estate companies in Kuwait and helps manage over 40 thousand units as for now.

Ajar is available in three different pricing plans. The basic one for USD 15 a month, but you need the Araj+ to use the best features of the app, such as auto-reminders, SMS notifications, payment tracking and analytics tools. There is also a custom plan for the most demanding customers.

liwwa

Country: Jordan and Egypt

Service type: peer-to-peer lending for small businesses

Ever wondered how to invest in small businesses? It used to be a tough question to answer. Small businesses don’t often even look for investors, because they don’t know how to reach them. But thanks to FinTech, now they can! liwwa has enabled thousands of local companies by offering them an easy way to find small-scale investors willing to bet their money. On the other hand, this startup allows everybody to make money helping local entrepreneurs, instead of empowering corporations even more. It’s all for greater good. All you have to do is top up your account, lend your money to a company of your choice and collect returns. Just remember to re-invest! But why would you do it this way, besides the ethical reasons? liwwa investments are usually very profitable – as the startup claims, the returns usually vary from 9.18% to 16.12% (with a median of 13.20%.)

The app has a brilliantly designed interface with advanced analytics tools, is Sharia law compliant and thanks to hundreds of data inputs, it calculates a pretty reliable risk score for all of your operations. Another pro of doing business with small businesses is that you can operate on small sums, so diversifying your investments is easy.

Tip of the iceberg

It’s always good to see how FinTech solutions work in favor of small, local businesses or just ordinary people, instead of just creating new sources of income for global corporations. And this is exactly what is going on in the MENA region. In order to pursue more of such cases, we’ve already covered green FinTechs. Check them out!