If you save or invest your money in more than one place, you may be annoyed with how bothersome it is to check and analyze what is going on with your assets, especially in real time. But logging into alt least three different platforms, checking the values, entering data into the spreadsheet is just pointless, when you can use asset management software. Read more to find out what it is and how it can make your life easier!

Before we talk about different examples of asset management software, let’s focus on the problems it solves, how investors managed before it was available and how open banking lets it do its job.

What was asset management like in the past

Just a few years ago, if a private investor wanted to control their financial assets in a precise way, they had to do everything manually. Literally, it meant checking all data in every system used and then putting it all together. It wouldn’t be that problematic in case of just a few sources of information that have to be analyzed, but if you invest on more platforms and have accounts in different banks, you may waste hours on getting it all together.

In order to solve this problem and automate the pointless waste of time, asset management software that can collect data from numerous sources, was invented. But it wouldn’t be possible without some way of accessing all of these databases belonging to different institutions and companies at once and without the need to manually log in to the systems. Fortunately, this problem was solved with the emergence of the open banking idea.

What is open banking and how it makes our lives easier

Simply speaking, open banking is concept that financial institutions should share certain information with third parties in a simple way. It can be achieved by the use of APIs that integrate banking systems with other applications and was made possible thanks to the

Payment Services Directive (PSD and PSD2), firstly introduced in 2007 by the EU. This act consists of a number of regulations that affect digital payments in UE and its purpose is to ensure security and confidentiality of data, as well as to integrate banking systems throughout the EU better. PSD is also the reason why you have to authenticate online payments with a credit card with a code or an app, as well as why multi-factor authentication is necessary when logging into your banking app.

For the sake of open banking and FinTech, the most important aspect, obviously, is that banks now have to share certain account data with regulated third parties. Asset management software, through API-based integrations that we mentioned before, can offer complex, all-in-one solutions for customers who, otherwise, would have no way to find so much information about their investments in one place.

Three levels of systems in asset management software

While the idea may seem simple, it is in fact quite complex, when it comes to practical solutions. Data, in asset management software, must travel through three levels of systems:

- Banking system

- An integrator

- Actual asset management software on a customer’s device

Why is the middle-man in a form of an integrator necessary and what is it, though? Building an API that is perfectly compatible with large-scale banking systems, provides security and operates in a stable way, while transferring huge amounts of important data is a monumental effort. Especially when it needs to be done from scratch and then maintained properly. This is why integrators (such as Plaid) exist and offer FinTechs ready-to-use APIs. The situation is no different than the one with ecommerce platforms or drop shipping APIs.

Top three asset management tools

For the sake of making sure we cover the topic thoroughly, but without delving too deeply into technicalities, let’s take a look at some examples of top asset management software available on the consumer market. To make it a bit spicy, we’re going to start with a free solution and compare it to more expensive ones. Let’s find out if it is worth it to pay for an asset management tool!

Intuit Mint – free and accessible

Mint is a very simple, yet powerful personal finance app. It’s also extremely powerful and offers a ton of features for free. First of all, it does everything a good piece of asset management software should do. With Mint, you can control all of your accounts, investments, credit cards and bills in one place. However, thanks to clever integration of innovative solutions, you get much more:

- Mintsights™ – an automatic system that finds new ways of saving money for you. It monitors your regular spendings and alerts you when you spend more on a given service or product than a month before. In other words, Mint, by analyzing your habits, finds opportunities to save.

- Automatic notifications about increases of subscription costs and when bills are due.

- Smart saving by planning budgets. The app automatically categorizes the transactions, so creating a budget is a breeze in Mint.

Besides these basic functionalities, Mint can help you find a financial product you need, as it offers a database of such products, where you can compare them.

Although Mint is extremely popular, it is not perfect. Users and media point out a number of common problems with this app. The most annoying seem to be problems with data synchronisation, especially when it comes to smaller banks, poor customer service (questions seem to stay unanswered for weeks), and very limited investing features.

All in all, Mint is a pretty solid and universal, free app (there are intrusive in-app ads, though).

YNAB – focused on psychology

You Need A Budget is a really clever name of an asset management app. The idea behind it is simple – you stick to the budget and save money. The company behind it claims that an average, new user saves $600 in the first two months, so even considering the costs (about $12 a month or $84 in an annual plan), it might be checking out.

In fact, YNAB is a complex saving and budgeting solution at its core and works best, when you stick to the three rules of the “YNAB strategy”:

- Give Every Dollar a Job – keep your discipline and allocate all of your resources to certain purposes in order to remove unrestricted spending.

- Embrace Your True Expenses – allocate money for large, but less frequent expenses (e.g. insurance, vacations, birthdays) on a monthly basis. Most of them are predictable, so stick to this rule to stress less.

- Roll With the Punches – adjust the budget when necessary, move money from one category to another and always go forward. Don’t let unexpected disruptions make you lose focus on the long-term goal.

As you can see, YNAB is a very specific product and it’s marketed as a solution for a very particular problem. Overall, then, this is not a general purpose asset management tool and doesn’t offer anything besides budgeting. Moreover, while its user base is already huge, it still only supports US/Canadian currencies. Will it be a good option, once it officially starts supporting GBP? Not as an alternative to Mint and other general purpose solutions, but as a complementary app – yes.

Quicken – a money powerhouse

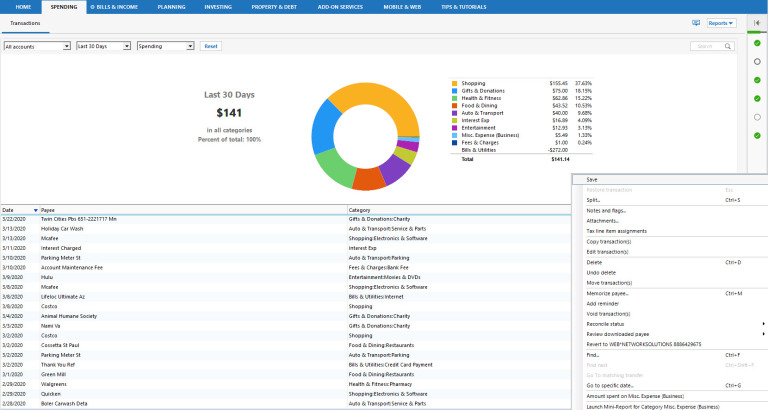

Quicken is one of the highest rated asset management software, according to the press. It’s not a surprise, considering it’s one of the longest developed tools, with over 25 years on the market. It’s main pro is being robust: this app can do almost everything, from planning a budget, through tracking transactions to investment analytics (with useful reports and graphs). Quicken supports multiple currencies, is available as a Windows or Mac application, can be accessed from a companion website and even allows you to do a number of things through a mobile app. All in all, it’s a whole ecosystem.

Quicken can look a bit intimidating at first glance, as it really is a powerful tool, but fear not, as setting it up is as easy as in case of Mint and other smaller apps. Just enter the usernames and passwords to your financial institutions and the app is ready. After that, you can get to tracking your personal income and spendings in a very detailed way and analyze it all easier thanks to colorful charts and graphs, you can add notes, flags, attachments, you can make sure every position is categorized properly, set up reminders about upcoming bills. Moreover, you can edit everything in a simple manner. The only lacking feature is paying bills directly from the app.

After you’ve made sure your Quicken is full of data, you can generate complex reports that will help you understand your situation better. And if you have any problem, the customer support is excellent, which is a huge pro, especially when you compare it to Mint’s slow and inefficient one and YNAB’s live-chat only policy.

Being a top top-notch piece of asset management system, Quicken cannot be cheap. And it is not, however, even in the most expensive Home & Business version, it doesn’t cost much more than YNAB, while offering a much larger set of features. It’s aimed at a different type of a customer though and an average YNAB user wouldn’t benefit from it much.

What will the future bring?

Since open banking is still a relatively new standard, asset management software is not uniform. There are small apps dedicated to a narrow set of functionalities, there are free, general purpose apps for a wide audience and there is a variety of complex solutions for those, who want to have everything under control. In case of asset management software development, sky’s the limit and there is a lot of space for new ideas on the market. Do you have one? Go ahead and turn it into a product!